Sivers: a critical node in the AI and CPO value chain - FREE

After analyzing the CPO supply chain, I found a company with enormous potential: every name on GlobalFoundries' list is worth tens of billions. Every name but one.

Analysis of Sivers Semiconductors: Introduction, Company Description, Earnings Season, Valuation, Risks, and Conclusion.

At the time of publication, SIVE is trading at SEK 31.52.

1-INTRODUCTION

Sivers Semiconductors is a small Swedish company with a $1B market cap that produces DFB lasers on InP substrates — the technology that allows data centers to replace copper with light. This is not an optional component. It is the physical chokepoint of CPO, the infrastructural transition on which NVIDIA, AMD, Google, and Amazon are betting billions. And in the entire world, the qualified players capable of producing it can be counted on one hand.

This is an analysis of a company that is still losing money, has a tight financial runway, and is worth 64 times less than its main competitor on the same GlobalFoundries supplier list. It is also, in my view, one of the most asymmetric risk/reward opportunities available today in the CPO ecosystem.

2-COMPANY DESCRIPTION

Sivers Semiconductors is a company engaged in the development and production of data transmission technologies, with a focus on semiconductor solutions used in high-performance communications. The company operates in areas related to both wireless connectivity and optical data transmission.

From a geographic standpoint, Sivers has an international presence. Headquarters are in Sweden, while research, development, and commercial activities are distributed across the United States, Scotland, and India. Revenue is generated primarily in Europe and North America, with a smaller share from Asia.

The two pillars of the business

The business is organized into two main segments:

1. Wireless: develops solutions based on mmWave technology, used in applications such as telecommunications, network infrastructure, defense, and satellite communications. This segment represents the largest share of revenue, with SEK 211.7M in FY2025.

2. Photonics: focuses on optical technologies for data transmission via light, including components such as lasers and solutions for data center and communications infrastructure applications. Segment revenue was SEK 92.4M in FY2025.

Within both segments, a significant portion of revenue comes from customer-specific development activities (NRE), which can subsequently evolve into larger-scale product sales.

Why SIVE is a chokepoint with high potential

In the photonics supply chain — from raw materials to hyperscalers — the laser component represents one of the most interesting chokepoints. It is the point where demand for bandwidth and energy efficiency translates directly into technological necessity.

Sivers is exposed to this layer of the value chain for three concrete reasons: it operates in a segment with few players and high technological barriers; it is already involved in projects that can evolve into production volumes; and it is growing its commercial pipeline by +64% to $453M, a signal of increasing customer interest.

3-EARNING SEASON Q42025

This quarterly report from Sivers did exactly what quarterly reports from transitioning companies do: it divided those who look at numbers from those who look at direction.

On the surface, a heavy miss. Q4 EPS at SEK -0.18 versus a consensus of SEK -0.13 (miss of -38.5%). The stock lost -8.05% the following day. If you stop here, the analysis ends badly.

But if you look at where those losses come from, the picture changes. In the fourth quarter, Sivers recorded SEK 31.0m in non-recurring costs in a single quarter: SEK 8.5m for a data security breach, SEK 11.9m for strategic projects, SEK 6.3m for restructuring, and SEK 4.3m for share option programs. Strip those out, and Q4 Adjusted EBITDA was SEK +10.8m — positive, and the best of the year.

The question, therefore, is not whether Sivers is losing money. It is. And it will continue to do so for several more quarters. The question is whether the market is looking at the wrong number — and whether the actual state of the operating business is far less deteriorated than the headline EPS suggests.

What worked

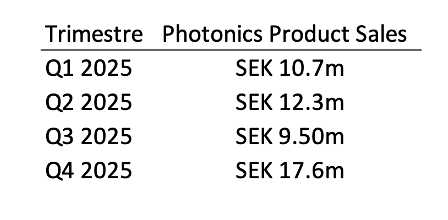

The most important number in the quarter is not the top line. It is Photonics product revenue: SEK 17.6m in Q4 2025, nearly tripled compared to SEK 7.3m in Q4 2024.

On a full-year basis, the Photonics segment nearly doubled its product revenue: SEK 50.1m in FY2025 vs. SEK 25.7m in FY2024. This is not noise. It is the signal that the transition from an NRE-dependent company to a product company is happening, at least in the laser segment.

Supporting this, the Wireless business grew 35% in 2025 and closed the year with a pipeline of $453M (+64% YoY). This is not a revenue number — it is a future number. Three European SATCOM vendors are at the RFP stage using Sivers-based solutions for the IRIS2 program. Tachyon Networks signed a production order worth $3M. The US Chips Act EW program completed its first year with "stellar execution," and the second-year contract worth $6.6M (+20%) is expected to be announced soon.

On the organizational front, the appointment of Raymond Biagan as Chief Revenue Officer in November is a concrete signal: you don't hire an industry-veteran CRO to manage the status quo. You hire one when you believe the pipeline needs someone who knows how to close.

What didn't work

Wireless product revenue collapsed to SEK 3.7m in Q4 (from SEK 17.8m in Q4 2024). The company explains that the mix shifted toward NRE — and this is technically correct, given that large defense and EW programs run primarily on development contracts. But the explanation doesn't eliminate the discomfort: a company that wants to transform into a product business cannot afford to let wireless product revenue hit historical lows in the same quarter it announces production orders.

Cash is the real point of vulnerability. At the end of December 2025, the liquidity position was SEK 29.7m in cash plus SEK 13.8m in restricted deposits — SEK 43.5m in total. With an operating burn of approximately SEK 14–15m per quarter in the core business (net of non-recurring items), the runway was tight. The refinancing with Bootstrap Europe for USD 17.0m, announced on February 24, 2026, eased the pressure — but didn't eliminate it. The structure of the new debt (USD 5m term loan + USD 12m convertible) implies potential future dilution if revenues don't accelerate on schedule.

Finally, the full-year EBIT of SEK -141.3m (vs. -127.1m) shows that operating leverage has not yet materialized despite 25% revenue growth. Total costs grew faster than the top line — the "other external expenses" line rose from SEK 100.8m to SEK 168.6m (+67%) and raw materials from SEK 62.8m to SEK 95.5m (+52%). This cost dynamic needs to slow before the model can demonstrate real scalability.

The number that actually matters

On an FY2025 basis, gross margin came in at 68.6% — a figure that doesn't get discussed enough. For a company generating 72% of its revenue from NRE and development, a gross margin of that size means the underlying business has a sound economic structure. The problem is not the product. The problem is the fixed cost structure and go-to-market investments that are compressing the path to breakeven.

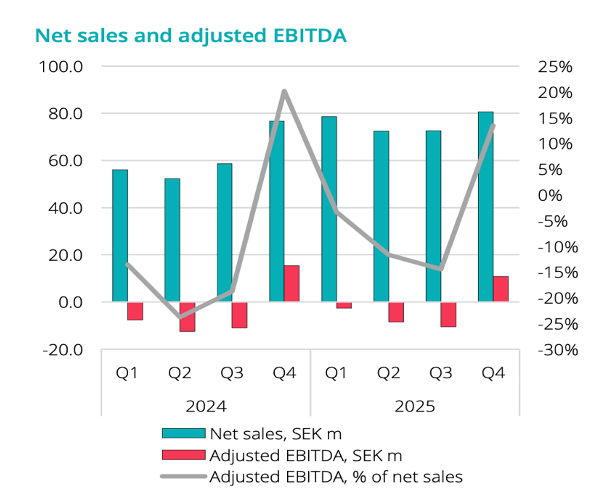

The annual Adjusted EBITDA sequence tells the same story more directly:

The direction is unequivocal. The pace of improvement — approximately SEK 5m per year in the recent period — is still too slow relative to the available financial runway. The qualitative leap must arrive in 2026, driven by pipeline conversion into concrete backlog and the start of Photonics production ramps.

4-VALUATION

With EPS negative through FY2027, a P/E ratio doesn't exist. I'm not using a DCF. I'm using the framework that makes the most sense for SIVE at this stage: ecosystem parity and catalyst sequencing.

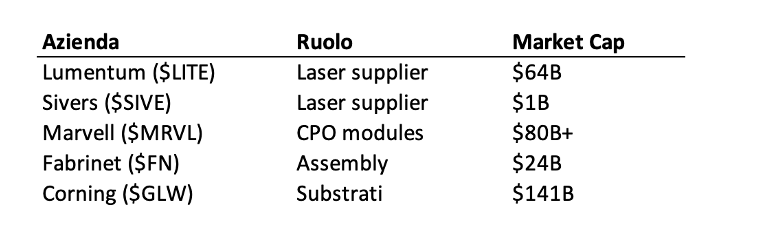

In March 2026, GlobalFoundries presented the official partner list of its CPO ecosystem at its investor webinar. It's a short list.

Every name on that list is worth tens of billions. Every name but one.

Two laser suppliers in the GlobalFoundries CPO ecosystem. Same list. Same end customers. One is worth 64 times the other.

This gap exists because the market has not yet priced what the recent catalysts are confirming one after another:

① Jabil 1.6T LRO — the most important. Jabil publicly confirmed the use of Sivers' DFB lasers for its 1.6T LRO modules. This is not an exploratory partnership — it is a confirmed design-in on a product ramping toward next-generation data centers.

② AMD + GFS CPO — the Ayar connection. AMD announced its CPO strategy with GlobalFoundries for the MI500 chip in 2027. Ayar Labs — in which AMD invested in the March 2026 Series E — already uses Sivers' DFB laser arrays in the SuperNova light source. If AMD uses Ayar for MI500, SIVE is already designed in.

③ Marvell / Amazon. Amazon has purchase agreements for "photonic fabric" from Celestial (Marvell). The laser supply chain reconstructed from SEC filings leads to SIVE.

④ NASDAQ listing. Sivers is proceeding toward a NASDAQ listing — the catalyst that unlocks liquidity, American analyst coverage, and institutional funds currently unable to buy a Stockholm-only listed stock.

My target is a $2B market cap.

It is built on a simple observation: there is no other laser company below $1B in the hyperscaler CPO ecosystem. All others are $10B+. Even discounting by 95% for size and execution risk relative to LITE, you arrive at $3B. $2B is the conservative target — it implies only that the market begins to price SIVE the way it has already priced every other name on the GlobalFoundries list.

Target Price: SEK 65

5-RISKS

Risk 1 — Financial Runway is the Real Bottleneck

This is the risk I monitor most closely. Not because the technology doesn't work — it does. But because the timing between cash going out today and cash coming in from production ramps is extremely tight.

At end of 2025, the liquidity position was SEK 43.5m in total. The Bootstrap Europe refinancing for USD 17m extended the runway — but the debt structure includes USD 12m in convertibles, meaning potential future dilution. Sivers already issued shares three times in 2025 for a total of approximately SEK 203m. Each new equity raise further dilutes an already significant base of ~311m shares.

If the JBL volume ramp and SATCOM production orders don't materialize into cash by H2 2026, the company returns to the market. A company that constantly needs to raise capital cannot build market confidence on fundamentals.

Risk 2 — The 2027 Laser Qualification Can Slip

The roadmap requires 5,000 hours of reliability testing — approximately 7 months — before any hyperscaler or transceiver manufacturer can commit to a production plan. If technical evaluations reveal issues with yield, linearity, or long-term thermal reliability, the qualification process extends.

Every month of slip pushes revenue back by at least a quarter. For a company with SIVE's runway, a one-year slip is the difference between being in position when the CPO supercycle accelerates and arriving too late. The 5,000-hour process is non-negotiable — it is a physical requirement of data centers, not a contractual preference.

Risk 3 — Multi-Sourcing Compresses Revenue Potential

Hyperscalers never buy from a single supplier. NVIDIA invested $2B in both Lumentum and Coherent — not one or the other. The concrete risk is that Lumentum — with $64B in market cap, an InP fab already expanding in San Jose, and direct NVIDIA backing — captures the dominant share of CPO production orders, leaving Sivers in a second-source role at lower volumes.

Second source doesn't mean irrelevant — it likely means real revenue, but materially lower than the bull case. If SIVE remains structurally at 20–30% of LITE's volumes, the re-rating toward $2B takes years instead of months.

6-CONCLUSION

Sivers sits at the exact point in the supply chain that cannot be bypassed. CW DFB lasers for CPO are not a commoditizable component — they require 25+ years of InP know-how, qualification processes that take months, and production capacity that worldwide counts only a handful of players. It's a physical chokepoint, not a contractual preference.

And Sivers is defending it with the right partnerships. Jabil for the 1.6T LRO modules. Ayar Labs — backed by AMD — with the SuperNova light source already designed in. POET Technologies for the Optical Engine. Marvell through Celestial. Doosan for SATCOM. The European Space Agency. DigiKey for broad market distribution. This is not a list of hopes — it is a list of signed agreements, issued production orders, confirmed design-ins.

The potential is enormous. The upcoming NASDAQ listing brings liquidity and American institutional investors who currently cannot buy SIVE. The CPO supercycle has just begun. The scarcity of qualified laser suppliers is structural.

The risks remain real: tight financial runway with potential dilution, a 2027 laser qualification that can slip, and a second-source role that limits volumes relative to the bull case. I don't ignore them.

But the probability distribution is asymmetric. The bull case is worth +106%. The bear case is already priced in at the February 2026 lows.

Rating: BUY. Target: SEK 65.

To download the analysis in PDF format:

This article is for informational purposes only and does not constitute financial advice. Investors should conduct their own research before making any investment decisions.

Le informazioni pubblicate da Daniele Cristaldi hanno esclusivamente scopo informativo e divulgativo. Nulla di quanto riportato costituisce consulenza finanziaria, sollecitazione all'investimento, né raccomandazione di acquisto o vendita di strumenti finanziari ai sensi del D.Lgs. 58/1998 (TUF) e della normativa MiFID II. Le analisi e le opinioni espresse riflettono unicamente il punto di vista personale dell'autore e non devono essere interpretate come garanzia di risultati futuri. Qualsiasi decisione di investimento è adottata dall'utente sotto la propria esclusiva responsabilità.