The Fed in a trap: oil, inflation, and the ghost of 2011 - FREE

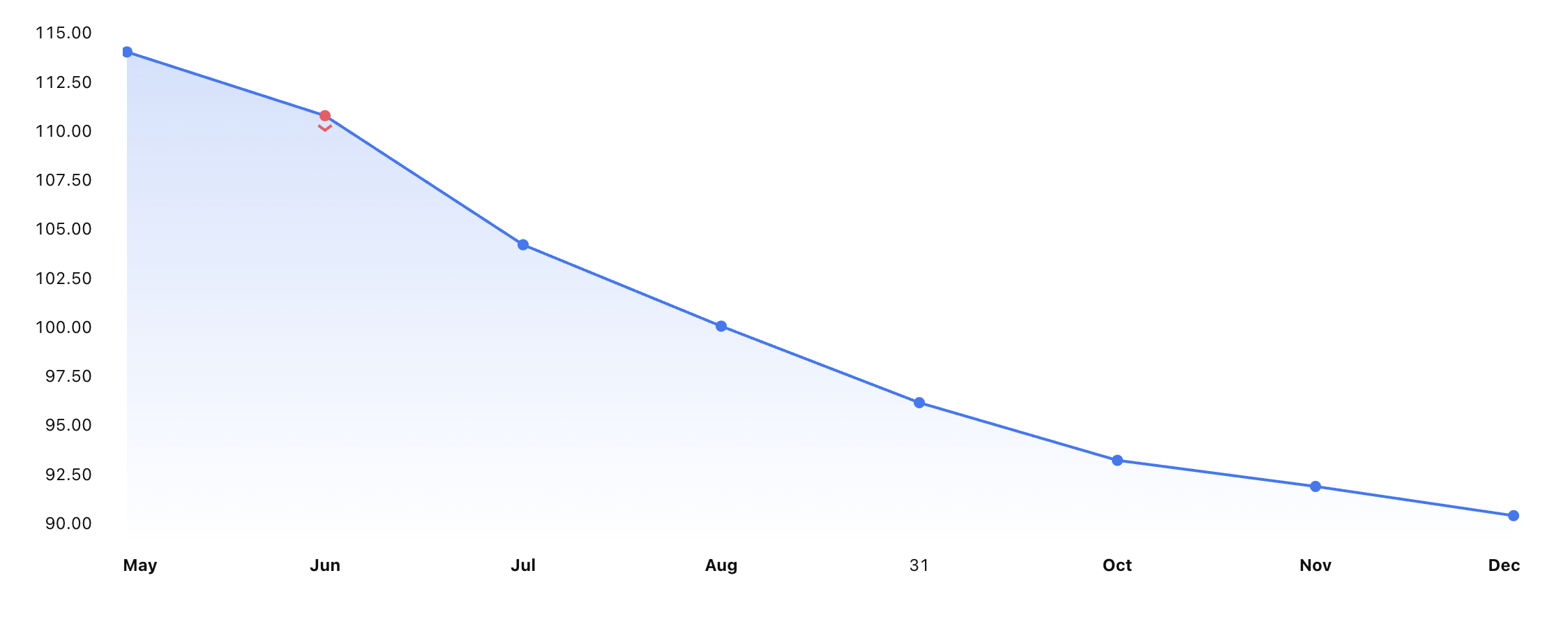

Technically, the market has priced in the end of the war. In practice, as of today, May 1 2026, the Strait remains closed and Brent is still trading at $114.

High oil prices do not weigh only on energy markets: they can fuel inflation, slow the path toward lower interest rates, and bring Europe back to the specter of a mistake already made in 2011.

The oil market tells an interesting story. Looking at the Brent forward curve (that is the prices the market expects over the coming months) the direction is clear: a gradual decline to around $90 per barrel by December 2026.

If this forecast proved correct, there would not be much to worry about. The spike in oil prices would be a temporary phenomenon, an external shock set to fade, without leaving lasting scars on inflation.

Inflation does not stem from a single cause.

It depends on a set of forces that interact with one another:

- Aggregate demand: when consumers and businesses spend more than the economy is able to produce.

- Supply of goods and services: production bottlenecks and shortages of raw materials.

- Monetary policy: the interest rates set by the Fed.

- Fiscal policy: government spending and fiscal deficits.

- Oil and commodity prices: which increase production and transportation costs.

- Labour market: higher wages combined with low unemployment raise costs for companies.

- Exchange rate: a weaker dollar makes imports more expensive.

Today, oil prices have risen because of the closure of the Strait of Hormuz: an external, sudden shock, not linked to excessive consumer spending.

Falling future price expectations confirm that the market reads this as a temporary event.

But what if the market is wrong?

Here is where the risk comes in. If the Strait of Hormuz were to remain closed longer than expected, or if it reopened under conditions different from those priced into futures, oil prices would not fall as the market currently expects.

The result would be persistent inflation, not transitory inflation.

And at that point, the Fed would face a difficult choice:

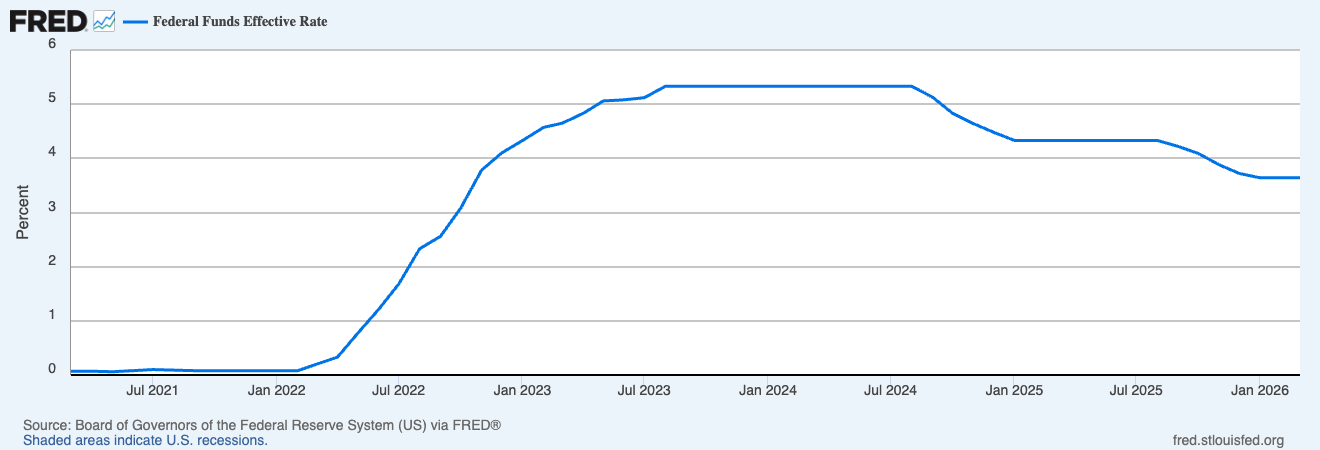

Before the crisis, in fact, the Federal Reserve had already started a rate-cutting cycle. A sensible choice in that context: lower rates stimulate credit, spending, consumptions. Exactly what policymakers do when they want to give the economy some breathing room.

The problem is that lower rates also tend to fuel inflation.

As long as elevated oil prices were not an issue, the Fed could afford to continue cutting rates. Not anymore.

It now finds itself squeezed between two opposing risks:

- Continuing to cut rates would mean adding fuel to an inflation rate already rising because of oil.

- Raising rates would mean repeating the same mistake the ECB made in 2011.

There is a near-perfect correlation between US oil prices and US CPI inflation, as shown in our below analysis.

— The Kobeissi Letter (@KobeissiLetter) April 2, 2026

As WTI crude surges above $112/barrel, we believe the US economy is bracing for 3.5%+ CPI inflation, particularly if current prices persist through April.

Asset… pic.twitter.com/WY1eN2ihzx

What happened in 2011?

It is worth pausing on that episode, because it is exactly the case that should not be repeated.

In 2011, Europe was in the middle of the sovereign debt crisis. Greece, Italy, and Spain were under pressure. The economy was fragile. In that context, inflation rose, not because consumers were spending too much, but because oil and commodity prices had increased.

The ECB raised rates twice. A decision that was technically understandable: inflation was rising, and the textbook response is to raise rates. But it was deeply wrong in context.Because there are two very different types of inflation:

- Demand-driven inflation: prices rise because people are spending too much. Raising rates makes sense: credit becomes more expensive, spending slows, and prices stabilise.

- Supply-driven inflation: prices rise because raw materials become more expensive. Raising rates solves nothing: the price of oil does not depend on interest rates. The only effect is to further choke an economy that is already under pressure.

The ECB had to reverse course just a few months later, but the damage had already been done.

As of today, the Fed knows that story well.

And it knows that current inflation has an external origin: oil.

But it also knows that if the oil shock were to persist, supply-driven inflation could turn into demand-driven inflation: expectations deteriorate, wages rise to recover lost purchasing power, and companies raise prices to cover higher costs. The contagion spreads.

The path is narrow. Cutting rates risks fuelling inflation.

Raising rates risks choking the economy over a problem that interest rates cannot solve. Staying on hold is the most prudent option, but also the one that requires the greatest courage, because it means admitting that the central bank, at this moment, has limited power.

Everything depends on how long the Strait of Hormuz remains closed.

Le informazioni pubblicate da Daniele Cristaldi hanno esclusivamente scopo informativo e divulgativo. Nulla di quanto riportato costituisce consulenza finanziaria, sollecitazione all'investimento, né raccomandazione di acquisto o vendita di strumenti finanziari ai sensi del D.Lgs. 58/1998 (TUF) e della normativa MiFID II. Le analisi e le opinioni espresse riflettono unicamente il punto di vista personale dell'autore e non devono essere interpretate come garanzia di risultati futuri. Qualsiasi decisione di investimento è adottata dall'utente sotto la propria esclusiva responsabilità.