Hormuz wasn’t just about oil: what did markets really price in? - FREE

I want to do a recap of everything that happened in the markets during the Iran–USA war, both from a geopolitical and a market perspective.

February 28, 2026: military strikes on Iranian territory by Israel and the United States. Why? Preventive attacks, Iran was rapidly increasing its missile capabilities. And, as is well known, Israel has always considered Iran an enemy.

Iran responds by attacking the UAE.

Two key considerations already emerge: AI, with Palantir, begins to enter the defense space as a central player. For the first time, the United Arab Emirates are attacked.

The Strait of Hormuz, a 30 km stretch of sea through which about 20% of global oil traffic passes, becomes central to the conflict.

Initially, ships stop transiting due to insurance constraints: since the strait is directly involved in the conflict, any vessel without specific war-risk coverage would not be reimbursed in case of cargo loss. At the same time, insurance companies suspend this type of coverage. Ships are therefore legally bound not to pass.

Within a few hours, Iran officially closes the strait, threatening to attack any vessel attempting to transit, effectively asserting control over that maritime passage for the first time.

In those same days, Ali Khamenei, Iran’s political and spiritual leader, is killed.

Now let’s move to a macroeconomic perspective and analyze the consequences.

Who is exposed to the oil flowing through the strait?

Asia: 80% of the oil passing through the strait is destined for China, India, and Japan:

India: imports 85% of its oil.

Japan: 90%.

China: theoretically the largest importer, but with alternatives such as Russia, Africa, and Latin America. Only 14% of Chinese oil comes from Iran.Europe: after the Russia–Ukraine war, it no longer relies on Russian oil, increasing its exposure to the strait.

How does the market react?

Brent jumps from $77 to $120 in just a few days.

Equities drop by 10%.

Bonds sell off.

And gold? Surprisingly, it falls by 23%.

A full risk-off across the board. The only asset holding up is the dollar, which starts to strengthen.

Technical note on gold: in 2025, gold had already risen by 65%, so institutions took profits and increased liquidity in response to market uncertainty. As a result, there was no classic flight to safe-haven assets.

The war continues but turns into a war of attrition: the cost for the U.S. to intercept Iranian drones ranges from $500K to $4M.

Cost of an Iranian drone? Around $35K.

It becomes an industrial problem.

The situation becomes increasingly difficult for the U.S. It almost looks as if the war started without a clear strategy, as if the possibility of Iran actually closing the strait had not been fully considered.

The United States effectively allowed Iran to take control of the Strait of Hormuz, which had previously been open to global shipping.

Now the U.S. is in a very challenging position: a costly war, traditional threat tactics followed by TACO seemingly ineffective against a politically entrenched country like Iran, markets reacting negatively, and mid-term elections approaching.

Donald Trump does not have a clear path to end the war while appearing victorious.

From here, things escalate:

On Saturday, March 21 2026 Trump posts on Truth Social that he would bomb all of Iran if the strait were not reopened (effectively declaring what would be considered a war crime by a sitting U.S. President).

Iran responds not only by refusing to reopen the strait but by attacking key U.S. strategic bases.

On Monday, March 23 2026 markets open with the 10-year Treasury yield at 4.5%, the 30-year at 5.0%, and the CBOE Volatility Index above 27.

With $39 trillion in debt, the U.S. cannot afford a market environment with rates at these levels.

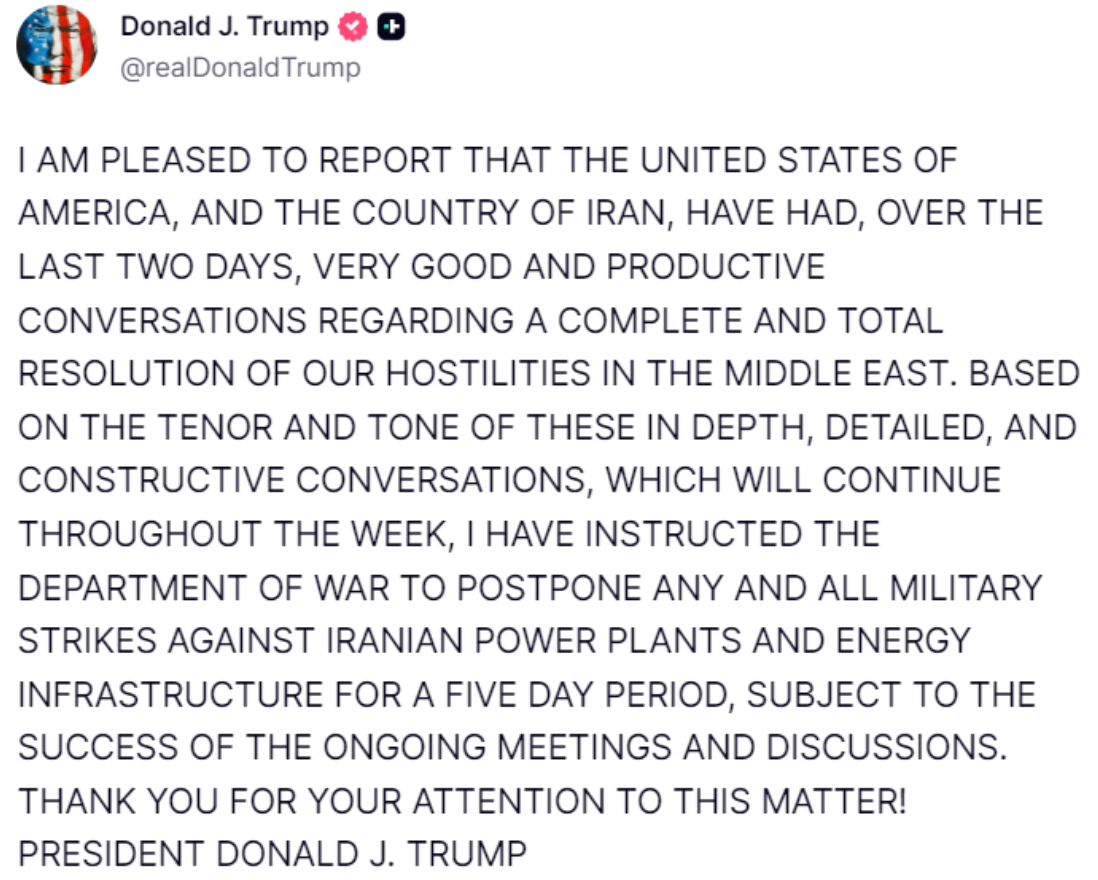

Then comes the epic taco:

A new post on Truth Social (deleted a few weeks later) claims that negotiations are going well.

Nasdaq +4.5%

Oil -15%

Gold rebounds from -10% to -1%

Meanwhile, 14 minutes before the post is released, someone buys $1.6 billion worth of Nasdaq (+0.4%), then sells shortly after the post, making a $60 million profit in just a few minutes.

In a conflict where the objectives appear increasingly blurred, it seems that neither the United States, now a net exporter of oil, nor Iran, which has consolidated its control over the Strait of Hormuz, is gaining a clear advantage.

By March 28 2026, it appears that the U.S. has no easy way out. The strait is effectively shut down and ships are not passing through. If ships do not pass, oil prices rise. If prices remain elevated for a prolonged period, inflation in the U.S. increases. Iran, on the other hand, responds to every provocation from Donald Trump, even portraying him as unstable, reinforced by denials regarding the supposedly positive progress of negotiations.

Heads-up: Pre-market so-called “news” or “Truth” is often just a setup for profit-taking. Basically, it’s a reverse indicator.

— محمدباقر قالیباف | MB Ghalibaf (@mb_ghalibaf) March 29, 2026

Do the opposite: If they pump it, short it. If they dump it, go long.

See something tomorrow? You know the drill.

March 30 2026: Donald Trump is under intense pressure. After the brief rebound on March 23, the market has fallen too much, mid-term elections are approaching, and Iran is not backing down from what appear to be erratic statements.

A combination of factors pushes the U.S. to bring the conflict to an end. Quoting: “the reopening of the strait is no longer a necessary condition to end the war.” The market breathes again and continues to recover over the following two weeks, pushing equities back above previous highs.

Now, some considerations that were overlooked during the conflict:

- This was the first time a country did not yield to Trump’s statements. By responding to the “provocations,” Iran showed that the United States may have been bluffing in previous cases. There is a theory suggesting that making extremely aggressive statements (such as threatening to attack all of Iran if the Strait of Hormuz was not reopened within 48 hours) can make other countries believe you are willing to go to any length. However, Iran saw through the bluff, and Trump backed down (“did the taco”).

- The issue of insider trading is becoming increasingly evident. It has always existed, and the example described in the article is just one case, but further investigation shows that on Polymarket, massive bets are often placed just minutes before an attack or a peace announcement.

- The role of China: perhaps the only real winner of this war was China, which never intervened and made no official statements. “Perhaps” because at a certain point even China started to feel the impact—neighboring countries dependent on Iranian oil reduced imports, and from whom do they usually import goods? China.

Another key point is how China views its partners more as resources than as allies, making it an unreliable counterpart. - Now, to the real insights: certain key market levels repeatedly triggered intervention from Trump via posts or “mini-tacos” to reassure markets.

Every time the 10-year Treasury yield rose above 4.5%, the 30-year above 5.0%, and the CBOE Volatility Index moved above 27–28, Trump stepped in to calm markets.Trump has lost political support, and mid-term elections may not favor him. He cannot afford to have markets turn against him as well, given that markets are heavily influenced by Wall Street, global funds, and political campaign financiers. - The United Arab Emirates, long considered a safe haven, were bombed—partly as a consequence of U.S. involvement—leading to a drop in real estate prices.

- Artificial intelligence is becoming increasingly embedded in warfare.

Le informazioni pubblicate da Daniele Cristaldi hanno esclusivamente scopo informativo e divulgativo. Nulla di quanto riportato costituisce consulenza finanziaria, sollecitazione all'investimento, né raccomandazione di acquisto o vendita di strumenti finanziari ai sensi del D.Lgs. 58/1998 (TUF) e della normativa MiFID II. Le analisi e le opinioni espresse riflettono unicamente il punto di vista personale dell'autore e non devono essere interpretate come garanzia di risultati futuri. Qualsiasi decisione di investimento è adottata dall'utente sotto la propria esclusiva responsabilità.