Semiconductors: from the chip to the supply chain - FREE

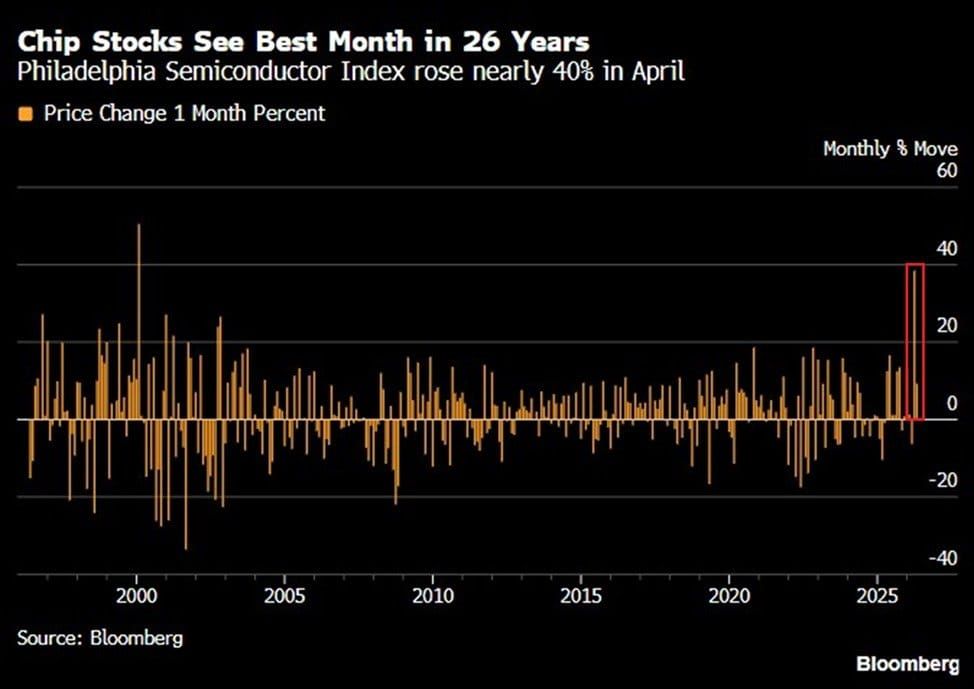

In recent months, the SOX, the semiconductor index, has risen by around 45%.

I wanted to understand what is behind these numbers: what semiconductors are, why producing them is so complex, where production is concentrated, and how the supply chain is structured.

A semiconductor is a material with properties between those of a conductor and an insulator. The most important one is silicon: abundant in nature, relatively stable, and suitable to be processed with extreme precision. On its own, however, silicon is not enough. To become useful, it must be purified, treated, etched, and transformed into a structure capable of controlling the flow of electric current.

The final product of this process is the chip.

A chip is a small piece of silicon, often as large as a fingernail, on which billions of microscopic devices called transistors are built.

Each transistor does one very simple thing: it switches between two states.

On = 1. Off = 0.

All modern computing starts from here. AI models, data centers, smartphones, electric cars, and industrial systems work thanks to sequences of 1s and 0s generated by transistors that switch billions of times per second.

There are different families of chips:

- Processing chips (CPU, GPU, ASIC): they process data.

- Memory chips (DRAM, NAND, HBM): they store it.

- Analog chips, sensors, and ADC/DAC converters transform physical signals (light, temperature, sound, movement, current) into digital information and vice versa.

In modern AI architectures, these categories work together: GPUs process, HBM memory feeds computation with enormous amounts of data, while optical components and advanced interconnections allow information to be transferred between servers, accelerators, and data centers.

The Scale of the Numbers

The complexity of semiconductors comes from scale. A modern transistor measures a few nanometers: one nanometer is one billionth of a meter. At these levels, producing a chip means working with extreme precision, where even a microscopic defect can compromise its functioning.

In 2025, the industry sold around 1.05 trillion chips worldwide, at an average price of around 0.74 dollars per unit. But this average hides the real point: most chips are worth a few cents or a few dollars, while a small share — especially those intended for AI, data centers, and advanced computing — can be worth hundreds or thousands of dollars.

This is the paradox of the sector: a few very high-value chips are driving a huge part of the growth. In 2025, global revenues reached around 792-796 billion dollars, up around 26% compared to the previous year. And with AI demand and the increase in memory prices, the industry is approaching the one-trillion-dollar threshold.

Why semiconductor manufacturing is so complex

- The first difficulty is the material.

Silicon is one of the most widespread elements in the Earth’s crust, but to build a chip, not just any silicon is needed. Ultra-pure silicon is needed, free from impurities at extremely low levels. Even microscopic contamination can compromise the functioning of the chip.

To this are added dozens of critical materials used in the different stages of production: gases, chemicals, metals, wafers, insulating materials, conductors, and special compounds. Some, such as gallium and germanium, are fundamental in specific high-value applications, including compound semiconductors, photonics, sensors, radio frequency, and dual-use technologies. Their refining chain is highly concentrated, especially in China, which has already used export controls as a geopolitical lever.

The risk, therefore, does not only concern the final demand for chips. It also concerns access to the materials needed to produce them. - The second difficulty is the machine.

To etch transistors onto silicon wafers, extremely advanced lithography tools are needed. In the most sophisticated nodes, the key machine is the EUV lithography system, meaning Extreme Ultraviolet. There is only one producer in the world: ASML, in the Netherlands.

The physical process is extreme. A tiny droplet of tin is made to fall in a vacuum, hit by very high-power lasers, and transformed into plasma. This plasma emits light at a wavelength of 13.5 nanometers. That light is reflected by mirrors with a precision almost impossible to imagine and used to etch microscopic patterns onto the wafer.

The most advanced EUV systems cost more than 300 million dollars each. ASML closed 2025 with around 32.7 billion euros in revenues and aims to reach 44-60 billion by 2030. Competition, in EUV lithography, effectively does not exist. Canon and Nikon compete in other areas of lithography, but today they are not real alternatives to ASML for the most advanced nodes.

This makes ASML one of the most important bottlenecks in the entire semiconductor industry.

Why production is concentrated in very few hands

An advanced chip factory can cost between 20 and 49 billion dollars. But capital, on its own, is not enough. The real competitive advantage comes from production experience: every wafer processed generates data, every mistake improves the process, every cycle increases yield. Those who produce more learn faster, and those who learn faster widen the gap with their pursuers.

For this reason, the production of the most advanced semiconductors is concentrated in very few hands. In frontier logic chips, those used for AI, data centers, premium smartphones, and high-performance computing, the absolute leader is TSMC. Samsung remains the main pursuer, while Intel Foundry is trying to re-enter the competition. SMIC, the main Chinese foundry, is strategically relevant but still behind the technological frontier, also because of the U.S. restrictions on access to EUV machines.

The real concentration is extreme: TSMC controls around 70% of global foundry revenues and a dominant share of the most advanced nodes. Many chips designed by NVIDIA, Apple, AMD, Qualcomm, and Broadcom are produced in Taiwan.

Semiconductor supply chain

It is necessary to distinguish between the different segments of the supply chain, because each one has different margins, risks, cyclicality, and competitive barriers:

- Fabless companies, such as NVIDIA, AMD, Qualcomm, and Apple Silicon, design chips but do not produce them directly. They have asset-light models, high margins, and strong exposure to final demand. Their competitive advantage comes from architecture, software, the ecosystem, and the ability to design increasingly high-performing chips.

- Pure-play foundries, such as TSMC and SMIC, produce chips on behalf of third parties. They are highly capital-intensive businesses, with enormous barriers, high cyclicality, and growing bargaining power in the most advanced nodes.

- IDMs, meaning Integrated Device Manufacturers, such as Samsung and Intel, design and produce internally. It is a more complex model: it requires enormous production investments, but also allows greater control over the technological roadmap. The problem is that, if production loses competitiveness, the entire model weakens.

- Equipment makers, such as ASML, Applied Materials, Lam Research, and KLA, provide the machinery needed for fabrication. In many segments, they operate in conditions of monopoly, duopoly, or strong technological specialization. For this reason, they can have high pricing power and resilient margins.

- Material suppliers, such as Shin-Etsu, Sumco, and Entegris, produce wafers, chemicals, and process materials. They are less visible to the general public, but fundamental for the production continuity of the entire supply chain.

- EDA and IP licensing, with companies such as Cadence, Synopsys, and ARM. Here the business is closer to software: design, simulation, verification tools, and proprietary architectures. They are fundamental assets because every advanced chip must be designed before it can be produced.

Le informazioni pubblicate da Daniele Cristaldi hanno esclusivamente scopo informativo e divulgativo. Nulla di quanto riportato costituisce consulenza finanziaria, sollecitazione all'investimento, né raccomandazione di acquisto o vendita di strumenti finanziari ai sensi del D.Lgs. 58/1998 (TUF) e della normativa MiFID II. Le analisi e le opinioni espresse riflettono unicamente il punto di vista personale dell'autore e non devono essere interpretate come garanzia di risultati futuri. Qualsiasi decisione di investimento è adottata dall'utente sotto la propria esclusiva responsabilità.